The good news at the start of 2023 quickly gave way to hints that the end of the year would be far less promising.

Over and above the risks that have already been mentioned many times, some of which continue to intensify (financial stability, social and political risks), we should bear in mind that the fight against inflation has not yet been won: excluding energy, inflation remains well above the targets set by central banks, while the situation on the oil market has (again) became tense following the attacks in Israel. All the leading indicators point to a sharp slowdown in activity in North America and the Eurozone towards the end of the year, and the recovery of the Chinese economy has rapidly collided with structural weaknesses and a lack of confidence among households and businesses. In this context, we have modified 7 country risk assessments (2 upgrades and 5 downgrades) and 33 sector risk assessments (17 upgrades and 16 downgrades), reflecting a degree of stability in our expectations over the next 18 months, in an environment that remains highly volatile and uncertain.

Towards a multipolar world

Beyond the persistence, and even intensification, of the Sino-American rivalry, several significant events in recent months have further upset the geopolitical landscape. The BRICS group expansion (Brazil, Russia, India, China, and South Africa) to include six new members (Saudi Arabia, Argentina, Egypt, UAE, Ethiopia and Iran), which some believe will mark the end of the predominance of the G7 and with it the post-war world order.

However, the ability of the BRICS+ to offer an alternative vision and take concrete steps to compete with the G7 is likely to remain limited (non-aligned objectives, tensions between China and India).

Inflation eases, but is not overcome

As anticipated in our previous Barometers, inflation has continued to recede "mechanically" in recent months, largely owing to energy and commodity prices below the peaks reached shortly after the invasion of Ukraine. Goods disinflation, linked to the rebalancing of demand towards the consumption of services and the return to normalcy of supply chains, is also ongoing.The signs that inflation is well entrenched remain and core inflation has been declining much slower in the advanced economies.Moreover, the risks that we mentioned regarding the resurgence of inflationary pressures towards the end of the year seem to be materializing, with oil prices trending upwards since the beginning of the summer.

The rhetoric that followed the decisions by the ECB, the Fed and the Bank of England (pause in rate hikes) all suggested that, while the tightening cycle may have ended,no rate cuts are expected in the coming months or even quarters.

Disappointing - and already over - recovery in China

China’s post-Covid recovery has been underwhelming, with economic data for both domestic demand and exports coming in soft.The widely expected rebound in consumption has been relatively weak as households were cautious, and the abandonment of the zero-Covid policy and the subsequent reopening of the Chinese economy only managed to provide an uneven boost to consumption patterns.

Investment has also been less of a growth driver for China as the private sector remained cautious towards fixed capital expenditure (notably due to real estate market, which continues to be concerning).

Appeasement for energy and agri-food in Europe

The changes in sector risk assessments this quarter were mostly in Europe, firstly in theenergy, agri-food and paper sectors. We are upgrading the energy sector in all Western European countries (excluding Germany), mainly because of higher margins for hydrocarbon producers and refiners. The agri-food sector in the region is also enjoying more positive momentum, unlike the paper sector, which is recording the highest number of downgrades.

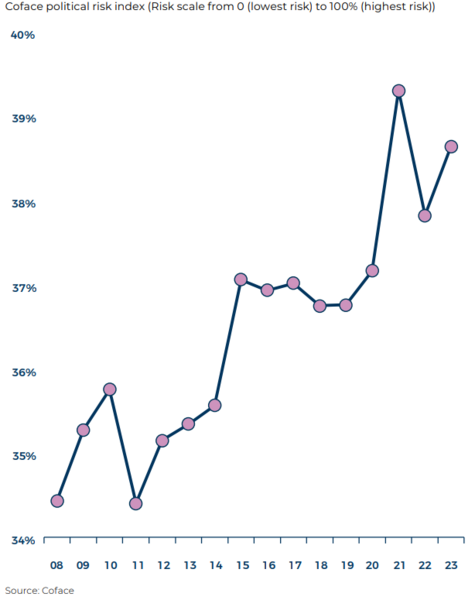

Mounting social and political risk is confirmed

Last year, following Russia's invasion of Ukraine, Coface warned of the risk of increased social risks due to rising prices for energy, basic goods and foodstuffs. When we updated our political risk indicator for 2022, we reiterated this warning. In this 2023 edition of the political risk indicator, our concerns are growing.The erosion of people's living conditions has given rise to new sources of frustration.

In recent years, political risk in its various forms and countries (Sri Lanka, Argentina, Niger, Gabon) has been a recurring theme in the news also for advanced economies (Israel, United-Kingdom, United-States). Social and political risk seems to be on the rise ina world that is becoming increasingly uncertain and unstablebecause of the reshaping of the global playing field and the perceptible emergency of climate change.

In terms of security,the number of conflicts increasedin 2022, with a particularly high death toll. If some conflicts have calmed down (Afghanistan, Yemen), others have emerged or become more intense as Nagorno-Karabakh in September, which highlights the persistent border crisis between Armenia and Azerbaijan.

In Africa, the number of active conflicts (state and non-state) on the continent has almost tripled since 2010.This trend is particularly linked to the fight against jihadist groups operating in Burkina Faso, Mali, Niger, Chad and Nigeria, for example This aggravated security context in the Sahel, and the difficulties in containing the Islamist insurgency since 2020, has also played a role in the recent political upheavals in the region. After Mali and Chad in 2021, and Burkina Faso (twice) last year, Niger experienced a coup d’état this summer.